A planning triangle may be familiar to anyone involved in managing or delivering projects. The three sides of the triangle represent the key aspects of a project: time, scope and cost. You can improve any two aspects, but at the cost of worsening the third. If you want to deliver more and faster then it will cost more. If you want to deliver more and cheaper then it take longer. And if you want to deliver faster and cheaper then you won’t be able to deliver as much.

If you try to deliver more and faster and cheaper, then either you’ll fail or the quality of what you deliver will suffer. Sometimes software companies rush a feature-rich product to market on a shoestring budget; it ends up being ridden with bugs.

Adapting the planning triangle

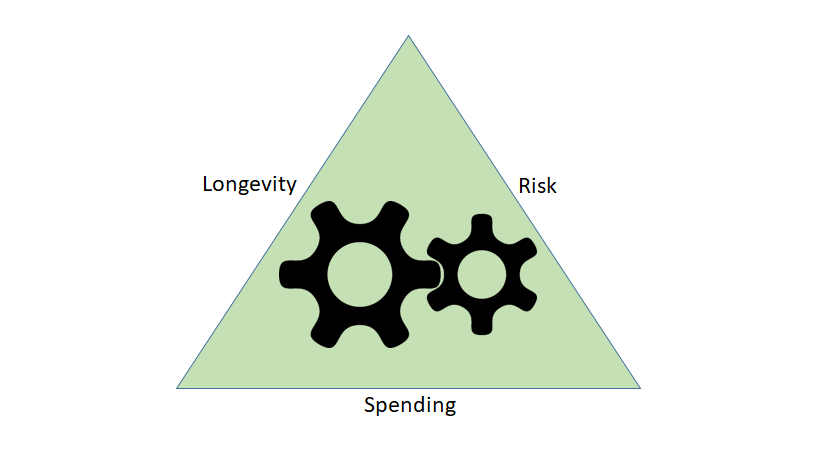

Retirement planning has its own planning triangle. The sides of the triangle are a bit different:

- Longevity. This represents your life expectancy.

- Risk. This means investment risk or volatility.

- Spending. The amount of money you can afford to spend, or leave as a legacy.

Just like for the project planning triangle, you can improve on any two aspects at the cost of the third. If you expect to live a long life (maybe you’re quite young) and wish to minimise investment risk, then you won’t be able to spend so much money. If you expect to live long and want to spend a lot, then you’ll need to take more investment risk. And if you want to spend a lot and minimise investment risk, then your money will stand less chance of lasting your whole life.

How to balance the retirement triangle

A professional financial planner can help interpret these competing goals and explore possible compromises that reflect your personal attitudes. You can also use EvolveMyRetirement to do the juggling using its intelligent strategy-generation algorithm.

Once this is done, your financial planner or adviser can then help with selecting investments and making adjustments over time.